Unlocking the Cash Value: How Whole Life Insurance Works as a Savings Tool

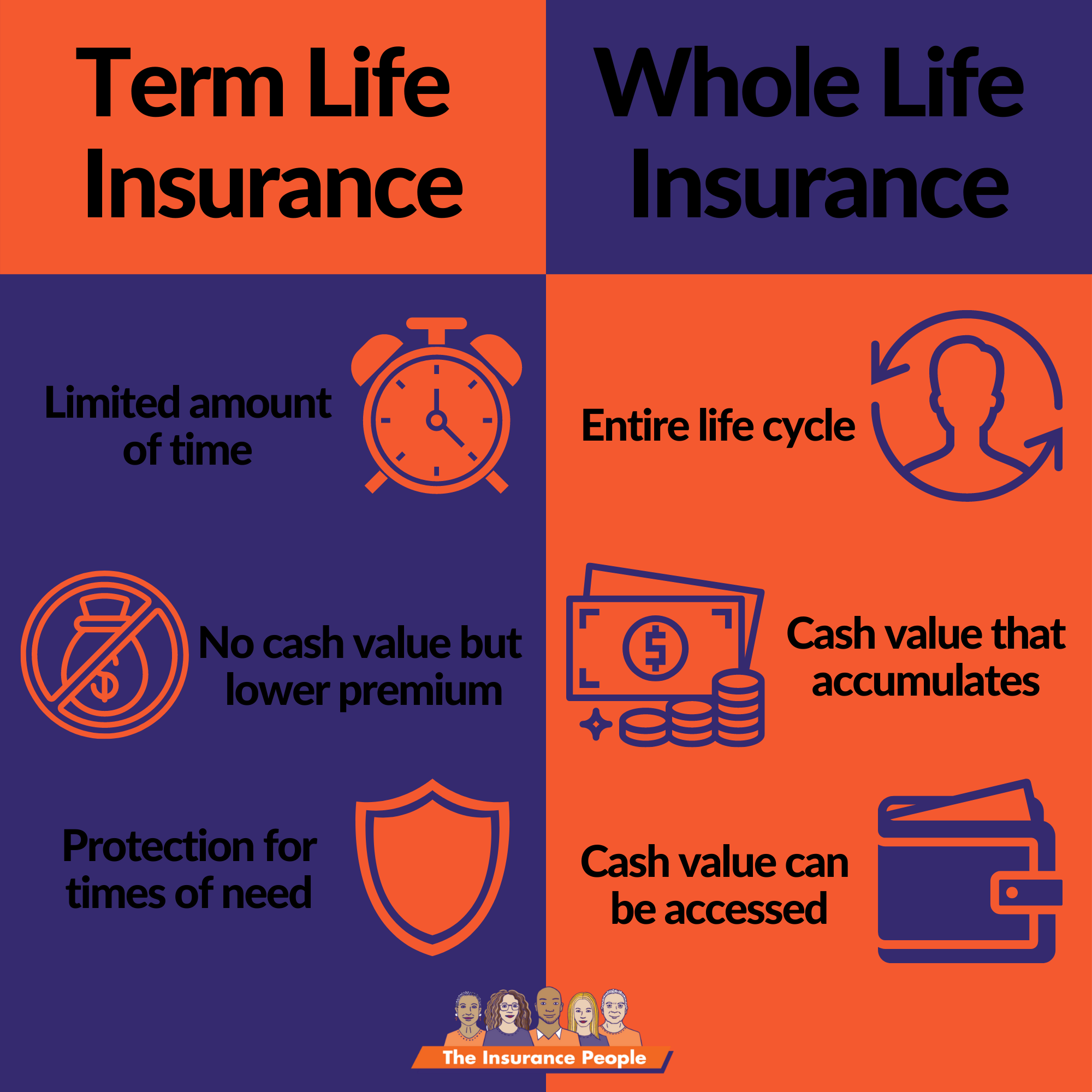

Whole life insurance is often viewed primarily as a safety net for loved ones, but many don't realize it also serves as a powerful savings tool. This type of life insurance policy accumulates cash value over time, acting as a financial resource that policyholders can access throughout their lifetime. The cash value grows at a guaranteed rate, allowing individuals to build wealth while providing lifelong coverage. Policyholders can borrow against this cash value, offering a source of funds for emergencies, large purchases, or even supplementing retirement income.

Understanding how whole life insurance works as a savings tool begins with recognizing its structure. A portion of the premiums you pay goes toward the death benefit, while another portion is allocated to build cash value. Unlike term insurance, which only provides coverage for a specific period, whole life policies ensure that your investment doesn't expire. Additionally, as the cash value grows, it can earn dividends depending on the company's performance, further enhancing your savings. This combination of guaranteed growth and potential dividends makes whole life insurance a unique and beneficial financial instrument.

The Advantages of Whole Life Insurance: More Than Just a Death Benefit

Whole life insurance offers a multitude of advantages that extend far beyond the typical death benefit. One of the most significant benefits is the cash value accumulation that occurs over time. Unlike term life insurance, which provides coverage for a specified period, whole life insurance combines life coverage with a savings component, allowing policyholders to build wealth. As premiums are paid, a portion goes toward the cash value, which grows at a guaranteed rate set by the insurer. This cash value can be accessed through loans or withdrawals, offering financial flexibility when unexpected expenses arise.

Moreover, whole life insurance provides permanent coverage, ensuring that your loved ones are protected no matter when you pass away. This peace of mind is invaluable; policyholders can rest assured that their beneficiaries will receive a death benefit to safeguard their financial future. Additionally, the premiums for whole life insurance remain level throughout the life of the policy, making it easier for individuals to budget for long-term coverage. The policy also typically includes options to earn dividends, which can further enhance its value, making whole life insurance an attractive choice for those looking for a comprehensive financial solution.

Is Whole Life Insurance the Right Choice for You? Key Questions to Consider

When evaluating whether whole life insurance is the right choice for you, it's essential to consider your long-term financial goals. Whole life insurance provides a death benefit along with a cash value component that grows over time. This makes it a unique product compared to term life insurance, which only offers a death benefit for a specified period. Here are some key questions to ask:

- Do you want lifelong coverage?

- Are you looking for a policy that can also serve as a savings or investment vehicle?

- Can you afford the higher premiums associated with whole life insurance?

Additionally, it's important to reflect on your current financial situation. While whole life insurance can be a solid addition to your financial portfolio, the commitment it requires might not align with everyone's budget. Consider the following aspects:

- Your age and health status, which can impact premium costs

- Your existing financial obligations, such as debt and living expenses

- Your appetite for risk and investment strategy

Ultimately, carefully weighing these factors will help you determine if a whole life insurance policy is the right fit for your needs.